Global TOMATO crop to be 41.8 m mT IN 2023

In February 2023, the World Processing Tomato Council estimated the global 2023 crop of tomatoes...

Back in late September 2021 we stated our belief that the supply chain crisis might persist until the middle of 2022.

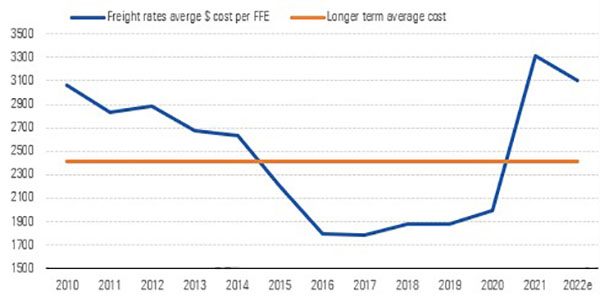

Full-year results from front-line shipping and logistics giants Maersk (MAERSK B) and DSV (DSV) have confirmed our thesis, with the former now believing that normalisation of shipping markets won’t take place until the second half of the year.

In the meantime, these companies are taking full advantage of tight capacity in shipping markets as a result of bottlenecks, with Maersk’s ocean business having delivered a return on invested capital of more than 45% in 2021, ahead of its long-term target of 7.5%, while the shipping industry as a whole has generated more profit in the last year than in the previous 10 years combined. While supply chain bottlenecks may subside in the second half of the year, causing downward pressure on freight rates, we fully expect another blowout year for shipping and logistics firms as these changes take time to filter through to the end client.

Additionally, the large shippers have been steadily converting clients to longer-term contracts, under the existential threat of the market driving rates higher and shipping capacity becoming harder to come by. Maersk expects 70% of volumes to be shipped under long-term contracts in 2022, up from less than half before the coronavirus, with most of these contracts locked in at relatively hefty freight rates. This effectively means much of the input cost inflation we’ve seen across consumer and industrial products will likely persist for some time.

The knock-on effects of the supply chain crisis have come to the fore recently, with commentary from companies as disparate as Tesla (TSLA), security provider Securitas (SECU B), and asset manager Abrdn (ABDN), all highlighting the disruption caused to end markets. It’s always darkest before the dawn, and while we believe the situation will improve in the second half of the year, we expect plenty more anecdotes of disruption to businesses between now and then.

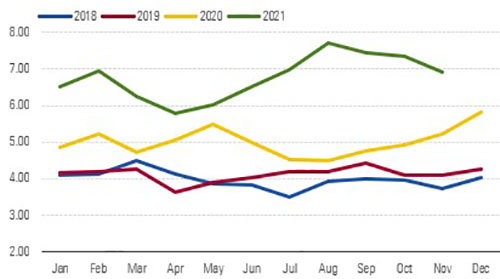

Ocean schedule reliability is barely registering any improvement in late 2021, while shipping delays (measured by average days) are still massively elevated relative to prior years.

This article first appeared in Morning Star